Raw material markets often experience prolonged downturns characterized by stubborn oversupply conditions. Producers typically maintain operations even when selling prices drop beneath production costs, banking on competitors exiting the market first.

The lithium sector is demonstrating this perfectly.

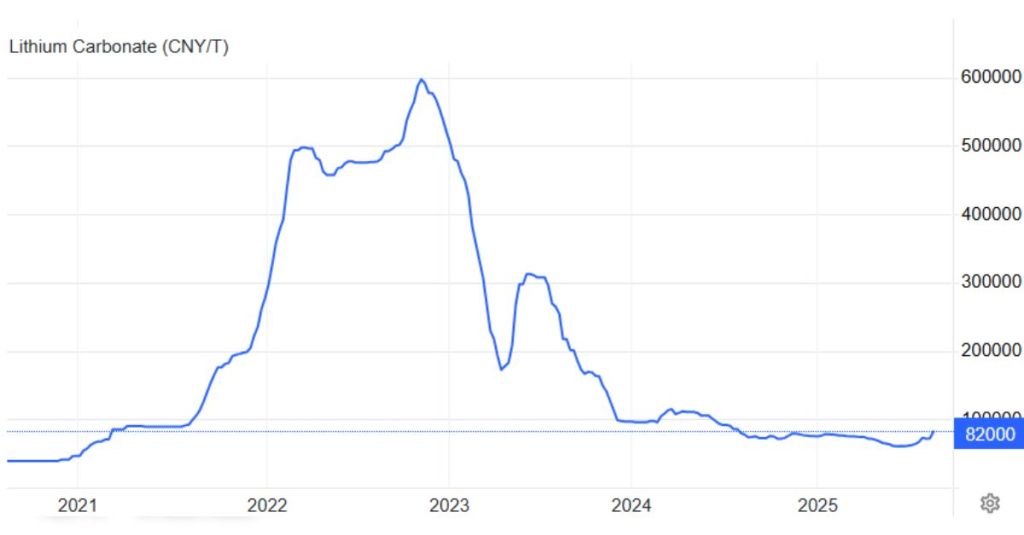

Lithium’s Dramatic Price Decline

Lithium spot prices have experienced a catastrophic price collapse, tumbling at one point more than -90% from peak levels reached in 2022 Q4. This downturn stems from two key factors:

- Excessive (Chinese) supply flooding global markets

- Electric vehicle adoption growing slower than anticipated

Current pricing leaves nearly half of worldwide lithium production operating at cash losses. Despite this, most operators continue running their facilities (while hoping for market recovery).

A Potential Market Catalyst

Monday brought significant news that energised lithium trading: Contemporary Amperex Technology (CATL), China’s battery manufacturing leader, halted operations at one facility following permit expiration. This development has propelled lithium prices upward of 26% since late June.

The closure carries substantial market weight given the facility’s output capacity. Morgan Stanley estimates the Jiangxi province operation was slated to deliver 58,500 tonnes annually – representing approximately 4% of global lithium supply. This volume roughly matches what analysts calculate as current market oversupply.

Broader Implications for Chinese Production

The shutdown has sparked speculation about China’s intentions regarding surplus capacity management. Supporting this theory, authorities recently ordered another operator, Zangge Mining, to cease production. These actions align with Beijing’s broader campaign against industrial overcapacity and destructive price competition across multiple sectors.

Reasons for Cautious Optimism

Several factors suggest the recent price surge may prove temporary:

Regulatory Uncertainty: CATL has indicated it’s pursuing permit renewal and expects minimal operational disruption, making the closure potentially short-term.

Inventory Overhang: Chinese lithium carbonate stockpiles have grown substantially, rising from 115,000 tonnes in January to 150,000 tonnes by May, according to Bernstein Data.

Planned Expansions: Scheduled capacity increases are projected to exceed demand growth throughout the current year.

Market Outlook and Recovery Prospects

While producers like Albemarle, SQM, Ganfeng Lithium, Tianqi Lithium, and Liontown Resources have seen share price gains following the news, sustained recovery depends on fundamental supply-demand rebalancing.

Price spikes often provide struggling producers temporary relief, potentially prolonging oversupply conditions if they encourage continued operation of marginal facilities.

The most promising path forward involves demand growth gradually absorbing excess capacity. Electric vehicle adoption outside China may eventually drive this recovery, though the timeline for lithium regaining its previous market strength remains uncertain.