Founded in Singapore in 2012, Grab sought to carbon copy the likes of super apps such as WeChat.

As a company it started out primarily looking to compete with Uber – and does so in many markets – however, it has also become the established go-to choice for not just ride hailers but for a plethora of different uses. Stylizing itself as the ‘Everyday Everything App’, the company also offers deliveries, insurance, payments, package sending.

It has also branched out to offer enterprise-grade solutions; such as those for fraud management as well as advertising opportunities.

In Southeast Asia, taxis or ‘Tuk-tuks’ are not always seen as a safe method of transport. It was with this idea that the founders of Grab came up with the concept of the company. This is especially the case in some markets such as Cambodia, where Grab is (still) the sole provider of ride-hailing services.

Grab’s Profitability: Key Metric Achieved

Grab has turned profitable, with the last four quarters achieving a positive net margin. This has led many analysts to upgrade their targets for Grab with the highest being – as of the publication date of this article.

In a further sign of positivity, the firm has recently completed a share buyback programme to the tune of $500 million.

A Positive Outlook

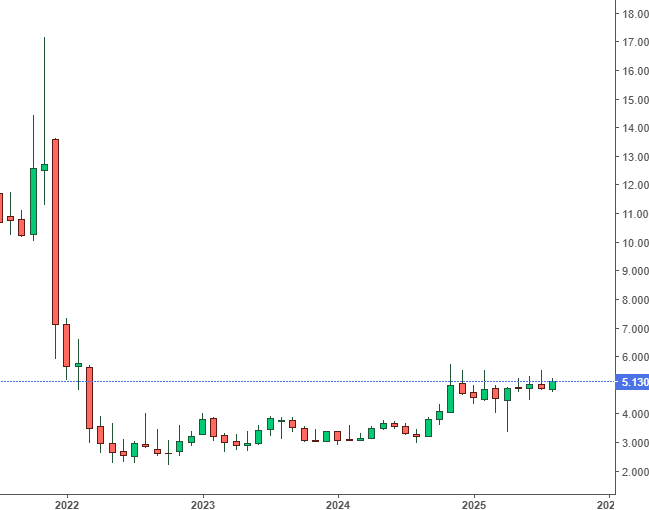

It is with this positive financial light that the firm has become a darling for analysts, with 25 analysts offering an average price target of 19%+ from today’s price of $5.12.

Although with the share price looking akin to RobinHood’s before its run up, a return to the ATL of $18 is not an impossibility.

The Speculatour’s Disclosure: Not financial advice. No guidance is provided for any particular investor, asset prices can fall as well as rise. The Speculatour is not a licensed securities dealer, broker, investment bank or advisor.